Europe’s IT services and BPM market is moving beyond isolated AI pilots into a coordinated build-out of infrastructure, skills and vertical use cases. This shift is set to structurally reshape deal flow over the next cycle. In European tech M&A, three fault lines will determine where value accrues: where AI compute resides, who controls data and workflows, and how quickly clients can rewire talent and operating models.

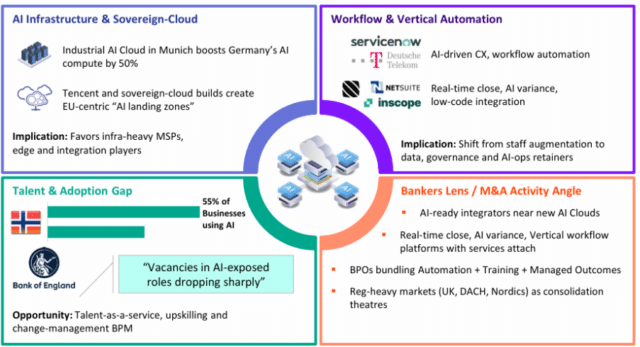

At the infrastructure layer, the build-out of sovereign and regionally anchored AI capacity is accelerating. Initiatives such as Deutsche Telekom’s Industrial AI Cloud in Munich and Tencent’s planned third data centre in Frankfurt are not just capex milestones; they are establishing sovereign AI “landing zones” that must be integrated, secured and continuously optimised. Alongside emerging sovereign cloud platforms like Polarise, this is tilting large transformation programmes toward providers that can combine hyperscaler expertise with strict European data residency and sector-specific compliance requirements.

Europe’s AI Services Stack: Where Bankers Should Look in 2026:

From a deal perspective, this is already driving increased strategic interest in mid-market managed service providers and integration specialists with strong Germany-centric or pan-European delivery footprints. Assets positioned close to these infrastructure clusters, with deep regulatory capability and hyperscaler partnerships, are likely to command valuation premiums as buyers prioritise proximity to AI compute and execution capacity.

At the application and workflow layer, enterprise value is shifting toward ownership of orchestration and decisioning. Finance and marketing are emerging as early adoption verticals for agentic automation. Platforms such as InScope and Stacks are re-architecting core finance processes, enabling near real-time close and dynamic variance analysis, while incumbents including Oracle NetSuite and Amdocs, through its GenAI partnership with Vodafone Germany, are moving to control orchestration across increasingly fragmented enterprise estates.

For IT services providers, this translates into a pivot away from legacy time-and-materials builds toward higher-value work across data engineering, control frameworks and ongoing AI model governance. In M&A terms, assets with embedded IP, workflow ownership or platform adjacency are likely to see stronger demand from both strategics and private equity, while pure-play implementation providers without differentiation risk margin compression and lower relative valuations.

The talent dimension remains the most fluid. Signals flagged by Andrew Bailey, including a decline in postings for highly AI-exposed roles, contrast with proactive upskilling initiatives from corporates such as Sainsbury’s. At the same time, markets like Norway, where enterprise AI adoption has more than doubled in a short period, highlight how quickly capability gaps can widen between AI-ready and AI-lagging organisations.

This divergence has direct implications for services models. Providers that can embed capability building, change management and operating model redesign into their offerings will be better positioned to shift from labour arbitrage toward outcome-based delivery and “talent-as-a-service” models. In turn, this is likely to drive consolidation around scaled platforms that combine technology, talent and delivery in an integrated manner.

Bringing these dynamics together, European IT services M&A is entering a phase where control of infrastructure access, workflow ownership and talent transformation will define competitive advantage. Buyers are expected to prioritise assets with proximity to sovereign AI infrastructure, differentiated capabilities in orchestration and governance, and demonstrable ability to deliver at scale in regulated environments.

Over the next 12–24 months, this should translate into premium valuations for specialised, capability-rich platforms, increased consolidation across sub-scale providers, and continued blurring of lines between IT services, software and data platforms. Firms that can align themselves to these three fault lines will be best placed to capture the next wave of value creation in European tech services.

Sources:

– Industrial AI and Managed AI: Germany’s leap into sovereign computing power

– More Norwegian businesses use AI – Nordic Labour Journal

– MWC 2026: Vodafone Germany Multi-Year Transformation Reaches Commercial Launch with Amdocs | Morningstar

– Andrew Bailey warns AI training is critical to future of UK jobs